Your Mortgage Is Not Just Debt - It Is a Financial Tool. Here Is How to Use It.

Is a mortgage good debt or bad debt?

A mortgage is, by most definitions, the most strategic form of debt a Canadian borrower can carry. Unlike consumer debt - which costs you money and gives you nothing in return - a mortgage finances an asset that historically appreciates in value, while simultaneously building your equity with every payment you make.

But the distinction between a mortgage that serves you well and one that simply costs you money comes down to one thing: structure.

A mortgage that is built thoughtfully, reviewed at renewal, and managed actively over its life will perform very differently than one that was signed and forgotten.

The Features Inside Your Mortgage That Most Borrowers Never Use

Canadian mortgage products come with a set of tools that are written into the contract but rarely explained at closing. Understanding these features is where the real financial advantage begins.

Prepayment Privileges

Most lenders allow borrowers to prepay a percentage of the original mortgage principal each year without triggering a prepayment penalty. This is typically between 10 and 20 percent of the original principal, depending on the lender and product.

On a $550,000 mortgage, a 10 percent prepayment privilege means you can put up to $55,000 toward your principal each year - penalty-free. Even more modest contributions, made consistently, can shave years off your amortization and save tens of thousands in interest over the life of the mortgage.

This privilege resets annually on most products. Borrowers who understand this use it strategically - applying tax refunds, bonuses, or one-time windfalls directly to principal at the right time of year.

Payment Frequency

The difference between monthly and accelerated biweekly payments is often underestimated. With accelerated biweekly payments, you make the equivalent of 13 monthly payments per year rather than 12. On a standard 25-year amortization, this single adjustment can reduce your total mortgage life to approximately 22 years, without any change to your rate.

This is a decision made once, at the start of the mortgage, that pays dividends for the entire amortization period.

Lump Sum Payment Options

Separate from prepayment privileges, many lenders also allow borrowers to increase their regular payment amount by a set percentage each year - often 10 to 20 percent above the original payment. Combining this with periodic lump sum contributions creates a compounding paydown effect that significantly accelerates the path to being mortgage-free.

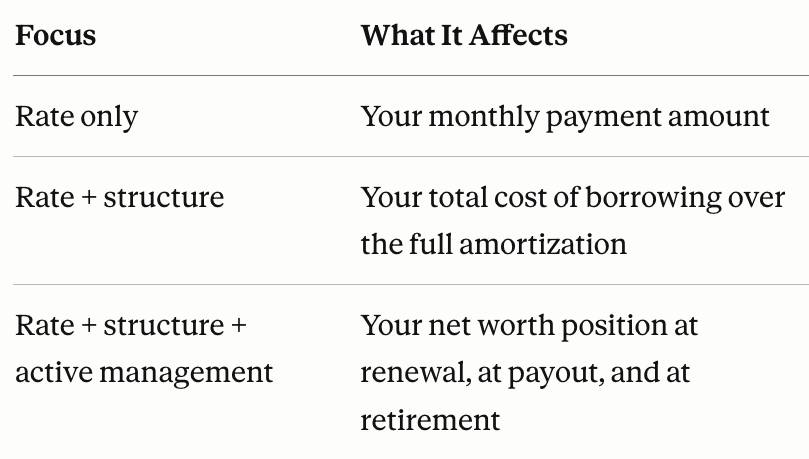

Does Mortgage Structure Really Matter More Than Rate?

Two borrowers with the exact same rate can end up with dramatically different outcomes depending on whether they used their prepayment options, chose the right payment frequency, and reviewed their mortgage at each renewal with the full market available to them - rather than simply accepting whatever their existing lender offered.

The Generational Dimension of Mortgage Strategy

One of the patterns that becomes visible over a long career in mortgages is that the families who are in a position to help their children with down payments today are, in most cases, not necessarily the families who earned the most. They are the families who managed their mortgage well.

Equity built through strategic prepayments, combined with property appreciation over 20 to 25 years, creates a financial position that extends beyond the original borrower. Whether that takes the form of a gifted down payment, a co-signing arrangement, or the gradual transfer of property, the starting point is almost always the same: a mortgage that was treated as a financial tool from day one.

This is not guaranteed, and it is not advice about whether to purchase property. It is an observation about the borrowers who tend to end up with the most options later in life.

Common Questions About Mortgage Prepayment and Strategy

What happens if I miss a prepayment opportunity in a given year?

Most prepayment privileges are use-it-or-lose-it within the calendar or anniversary year, depending on the lender. They do not carry forward. This is why timing matters - and why working with a broker who tracks these windows for you can make a real difference.

Can I change my payment frequency after signing?

In most cases, yes - though some lenders have restrictions on how often and when you can make changes. This is worth confirming before signing, not after.

Is it better to put extra money toward my mortgage or invest it?

This is a personal finance question that depends on your interest rate, your investment return assumptions, your risk tolerance, and your tax position. There is no universal answer. What I can tell you is that for most Canadian borrowers with a mortgage, the guaranteed return of prepayment at today's rates is worth serious consideration.

What is the stress test and does it affect how I manage my mortgage after closing?

The stress test, governed by OSFI guidelines for federally regulated lenders, determines whether you qualify for a mortgage by testing you at a rate higher than the one you are actually receiving. It applies at approval and does not directly affect your day-to-day mortgage management after closing. However, it is relevant again at renewal if you are switching lenders.

Does this apply to variable rate mortgages as well?

Yes. Prepayment privileges and payment frequency choices exist in both fixed and variable rate products, though the specific terms vary. Variable rate borrowers have additional considerations around conversion options and the timing of rate moves, which is a separate but related strategic conversation.

Practical Tips for Getting More From Your Mortgage

Review your prepayment allowance each year and put any available surplus toward principal before the window closes. Ask your broker what your specific prepayment terms are - not all products are the same. Choose accelerated biweekly payments at signing if your cash flow supports it. At every renewal, review the full market - not just your existing lender's offer. Understand your penalty structure before making any changes mid-term.

If you want to talk through how your current mortgage is structured - or what a new mortgage could look like with these tools built in from the start - I am happy to walk through it with you. Book a call at www.MortgageCall.ca or email [email protected].