What Is a Mortgage Penalty in Canada, and How Much Could It Actually Cost You?

Most Canadian borrowers spend a significant amount of time comparing mortgage rates before they sign. Very few spend the same amount of time understanding what it will cost to exit that mortgage before the term ends.

That conversation matters more than most people realize. And it is one that tends not to happen at the bank.

The short answer: A mortgage penalty is a fee your lender charges if you break your mortgage before the end of your term. The amount depends on your mortgage type, your lender, and - critically - where interest rates are at the time you want to leave.

Why Do Mortgage Penalties Exist?

When a lender offers you a fixed rate for five years, they are making a commitment. They are pricing your loan based on current market conditions and taking on the risk that rates will move. If you exit early, the lender may lose the income they anticipated. The penalty compensates for that loss.

For variable rate mortgages, the penalty is typically simpler. For fixed rate mortgages - especially at major Canadian banks - the calculation is more complex, and in many market conditions, considerably more expensive.

How Are Canadian Mortgage Penalties Calculated?

There are two main penalty methods in Canada.

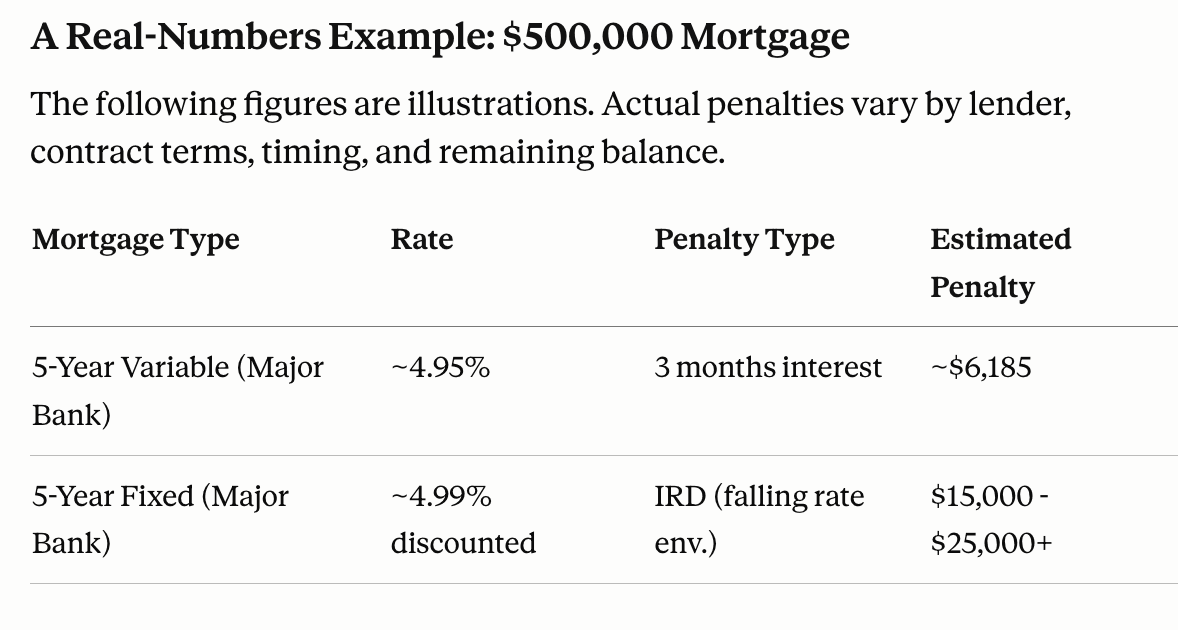

Three Months Interest This is the standard penalty for variable rate mortgages and is often the baseline for fixed rate mortgages as well. It is calculated using your outstanding mortgage balance, your current rate, and three months of interest at that rate.

Interest Rate Differential (IRD) This is specific to fixed rate mortgages and is calculated based on the difference between your original rate and the rate your lender can now offer for the remaining term. The lender uses this difference to estimate what they would lose by releasing you from your contract.

For fixed rate mortgages, the penalty is the greater of three months interest or the IRD.

The Big Bank IRD Problem

Here is where things become important. Major Canadian banks typically calculate the IRD using posted rates rather than the discounted rate you actually received. This creates a wider gap than most borrowers expect.

As rates fall, the differential between the posted rate used in your contract and the current posted rate widens. The result: the more rates drop, the higher your penalty grows. The market gives you a lower rate and simultaneously makes it more expensive to access it.

This is not a glitch. It is how these contracts are written. And it is information that rarely surfaces clearly before signing.

The variable rate penalty is predictable and, while not small, is a number most borrowers can plan around. The fixed rate IRD penalty in a falling rate environment is a different conversation entirely.

What Else Is Included in Your Exit Costs?

The penalty is the largest line item, but it is not the only one. A full exit cost picture for a Canadian mortgage may include:

Discharge Fee: A lender's administrative fee to release the mortgage from title. This typically ranges from a few hundred dollars to around $350, depending on the lender. It is not a penalty, but it is real.

Reinvestment Fee: Some lenders charge this as a flat fee in addition to or instead of an IRD, particularly mono-line lenders. Reading your commitment carefully matters here.

Porting Restrictions: If you plan to carry your mortgage to a new property rather than breaking it, your ability to do so depends entirely on what your contract allows. Some lenders have strict timelines, portability conditions, or top-up restrictions that can make porting impractical.

Cash Back Repayment: This is the one that surprises people most consistently. If you took a cash back mortgage - where the lender provided a lump sum at signing in exchange for a higher rate - you may be required to repay all or a portion of that cash back if you break the mortgage early. Some lenders prorate the repayment based on time remaining. Others require the full amount back regardless of timing, even if you leave one day before maturity.

Frequently Asked Questions

Can I avoid a penalty if I wait until the end of my term? Yes. If you let your mortgage mature naturally, no prepayment penalty applies. You are free to renew, transfer to a new lender, or refinance without penalty at that point.

What is the difference between breaking a mortgage and transferring it? A transfer (also called a switch) moves your mortgage to a new lender at renewal without triggering a penalty. It is different from breaking your mortgage mid-term, which does trigger the penalty. Transfers at renewal are penalty-free and are one of the most underused tools Canadian borrowers have.

Does the penalty go away if I port my mortgage? In most cases, yes. Porting means carrying your existing mortgage to a new property rather than discharging it. If your contract allows porting and you meet the lender's conditions, no penalty applies. However, porting rules vary significantly by lender, and the window to complete a port is usually limited to 30 to 90 days.

Does it ever make sense to pay the penalty? Sometimes. If the rate savings over the remaining term exceed the penalty cost, breaking can make financial sense. This calculation requires comparing the new rate, the amount of time left, and the full penalty figure. A broker can run this math for you before you decide.

Are penalties the same at all lenders? No. Credit unions, mono-line lenders, and Schedule B lenders often calculate IRD differently than major banks. Some use the discounted rate as the reference rather than the posted rate, which can result in a considerably smaller penalty. Lender selection is not just a rate decision. It is a structure decision.

Practical Tips Before You Sign

- Ask your broker to explain the full penalty calculation methodology for any mortgage you are considering, not just the rate.

- If a cash back incentive is part of the offer, understand the full repayment terms before accepting it.

- Request a disclosure of all exit-related fees: penalty, discharge, reinvestment, and any portability conditions.

- If you anticipate a life change within the next five years - a move, a growing family, a business income shift - factor the cost of exiting early into your product choice.

- Variable rate mortgages at most lenders carry a simpler, more predictable penalty structure. That predictability has real value in certain situations even when the rate is slightly higher than a fixed alternative.

The Bottom Line

A low entry rate is worth pursuing. But the full cost of a mortgage includes how much it costs you to leave it. Understanding both sides of that equation - entry and exit - is how you build the lowest total cost of borrowing, not just the lowest payment on paper.

If you are reviewing a mortgage commitment and want to understand what you are committing to beyond the rate, we can definitely talk on the phone.

Book a call at www.MortgageCall.ca or email [email protected]

Snezhana Todorova is a licensed mortgage broker with BRX Mortgage (Lic 13463), serving clients in Guelph, Ontario and virtually across Ontario.